Categories

Real EstatePublished April 4, 2026

Protecting Your Home After Closing: What Eastside Seattle Homeowners Should Know

What Eastside Seattle Homeowners Should Do Right After Closing — Protecting Your Mortgage, Your Family, and Your Future

You did it. You closed on your home on the Eastside of Seattle.

Maybe it's a craftsman in Kirkland with a view of the lake. A newer build in Sammamish with top-rated schools around the corner. A sleek contemporary in Bellevue minutes from the tech corridor. Whatever the address, you've made one of the most significant financial decisions of your life — and you should feel proud of that.

But here's the part that doesn't make it into the congratulations cards:

The moment you close, you also take on a six — sometimes seven — figure financial obligation tied to your name. And most new homeowners spend so much energy getting to closing that they never stop to ask: What happens if something goes wrong?

This post isn't meant to dampen the celebration. It's meant to protect it. Because the Eastside homeowners who build lasting wealth aren't just the ones who buy smart — they're the ones who protect what they buy.

(Important note: This is not financial or insurance advice. Everything here is meant to spark a conversation with a licensed financial advisor or insurance professional who can guide you based on your specific situation.)

Why This Conversation Matters More in the Eastside Market

Before we get into specifics, it's worth understanding the stakes.

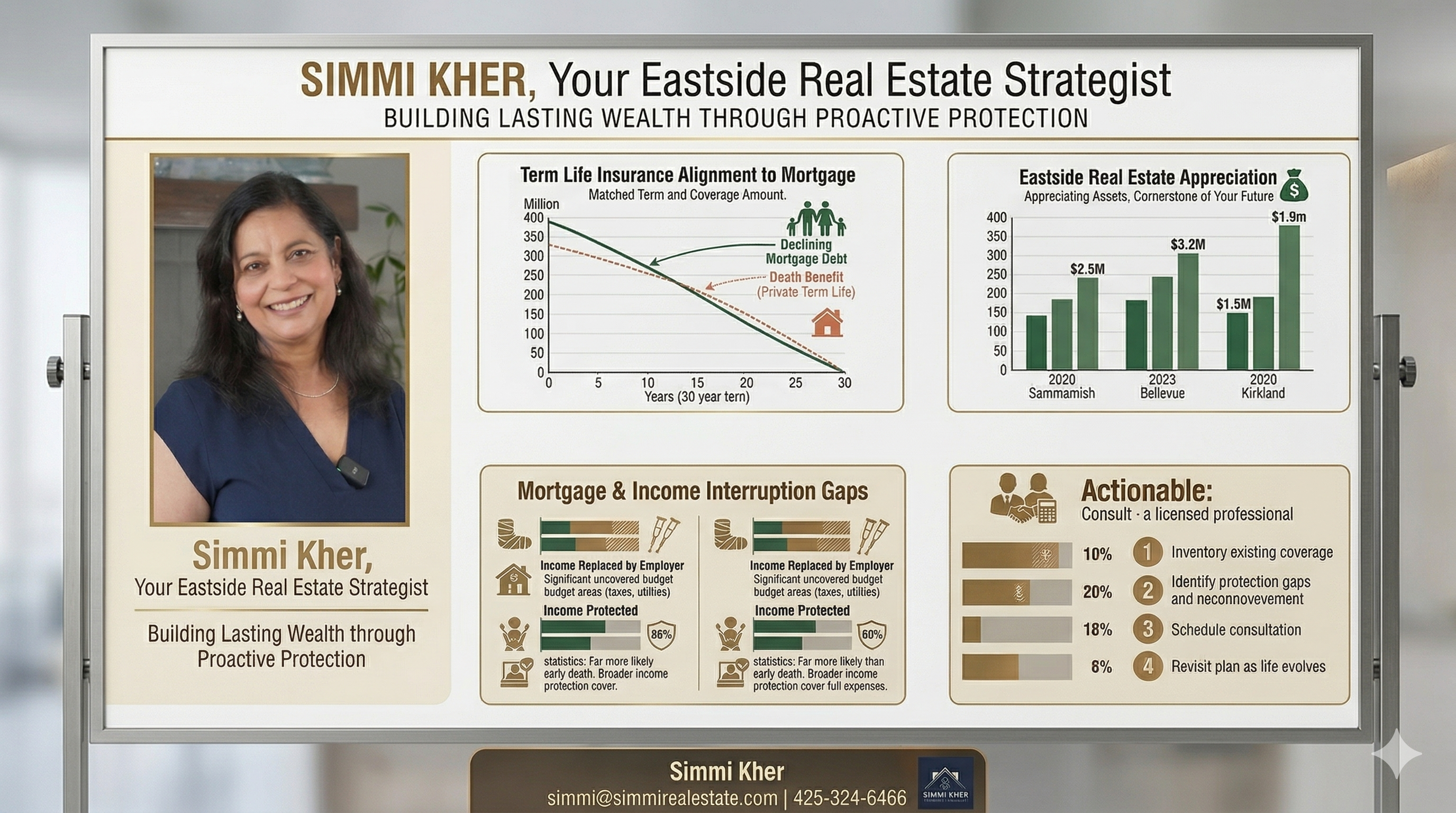

The Eastside of Seattle — Bellevue, Sammamish, Kirkland, Redmond, Issaquah — is one of the most expensive real estate markets in the country. Median home prices in many of these cities regularly exceed $1 million. That means the mortgage most homeowners carry here is not a small liability. It's a financial commitment that will likely shape your household budget for the next 20 to 30 years.

For many families, their Eastside home will become their single largest asset. As property values appreciate over time — and historically, Eastside values have done exactly that — that home becomes the cornerstone of their financial future. Their retirement. Their kids' inheritance. Their safety net.

That's why protecting it isn't optional. It's essential.

And yet, shockingly few new homeowners ever sit down to ask: What financial protections do I have in place if I can't make this mortgage payment?

Two Protections Worth Exploring With a Licensed Professional

1. Term Life Insurance — Matched to the Length of Your Mortgage

Here's a scenario most people don't want to think about but every homeowner should:

You pass away unexpectedly. Your spouse, your partner, your family — they inherit your home. But along with the keys, they inherit whatever remains on the mortgage. In the Eastside market, that could easily be $700,000, $900,000, or more, still owed to the lender.

Without a financial plan in place, your loved ones now face a painful choice: find a way to cover that payment on a single income, or sell the home — possibly in a rushed timeline that doesn't favor them financially.

Term life insurance is one of the most straightforward tools to address this risk. The concept is simple: you purchase a policy that aligns with the term of your mortgage — typically 15 or 30 years — for a coverage amount that reflects what you owe. If you pass away during that period, the death benefit can be used to pay off or significantly reduce the remaining mortgage balance.

For a relatively modest monthly premium, your family gets the ability to stay in the home. No forced sale. No financial pressure layered on top of grief. Just security.

A few things worth discussing with a licensed insurance professional:

- How much coverage do you need? A common starting point is coverage equal to your outstanding mortgage balance, though many financial planners suggest factoring in other debts, income replacement, and future expenses as well.

- What term length makes sense? Many homeowners choose a term that mirrors their mortgage — but your individual situation may call for a different approach.

- How does your existing coverage stack up? If you have life insurance through your employer, it may not be sufficient — especially for Eastside homeowners carrying large mortgage balances.

2. Mortgage Disability and Income-Protection Coverage — The One Most Homeowners Have Never Heard Of

If term life insurance is the conversation most homeowners eventually have, income-protection coverage is the one most people skip entirely. That's a significant gap — because statistically, you are far more likely to experience a disabling illness or injury during your working years than you are to die.

Think about what that means for a homeowner.

You're injured in a car accident and can't work for six months. You're diagnosed with a serious illness that keeps you out of work for a year. Your income stops — but your mortgage doesn't. Your property taxes don't. Your utilities don't. Life doesn't pause because your paycheck did.

This is exactly the scenario that mortgage disability insurance and income-protection (disability) coverage are designed for. These are distinct products — worth understanding the difference:

- Mortgage disability insurance specifically covers your mortgage payment if you become unable to work due to a qualifying illness or injury. The benefit is typically paid directly to your lender, keeping your loan current while you recover.

- Income-protection or disability income insurance is broader — it replaces a portion of your overall income (typically 60–70%) during a period of disability. This gives you flexibility to cover not just your mortgage, but your full household expenses.

For Eastside homeowners — where mortgages are large and cost of living is high — either of these products can be the difference between weathering a difficult period and losing the home entirely.

Questions to explore with a licensed professional:

- Does your employer offer short-term or long-term disability coverage? If so, is it enough to cover your mortgage in this market?

- What is the elimination period on the policy — how long do you have to wait before benefits kick in?

- What qualifies as a "disability" under the policy?

- How does the benefit interact with other income sources?

The Real Cost of Being Underprotected in a High-Value Market

Let's be direct about something: in a market like Sammamish or Bellevue, the financial gap between "covered" and "uncovered" is enormous.

If a homeowner in a lower-cost market loses their income temporarily and needs to sell, they might walk away with modest equity and find an affordable rental in the interim. For an Eastside homeowner, a forced or distressed sale — timed poorly, executed under financial pressure — can mean leaving significant equity on the table. It can mean uprooting a family from schools, neighborhoods, and community connections they've built.

The Eastside market rewards patience and long-term ownership. The homeowners who build real wealth here are the ones who can hold on through life's inevitable disruptions — because they planned ahead.

How to Start the Conversation

If you've recently closed on a home on the Eastside of Seattle and haven't yet reviewed your financial protection picture, here's a simple starting framework:

- Inventory what you already have — Life insurance through your employer, any existing disability coverage, your emergency savings, and your household budget margin.

- Identify the gaps — What would happen if your income stopped for 3 months? 6 months? 12 months? Could you cover your mortgage without your primary income?

- Schedule a consultation with a licensed professional — A fee-only financial planner or an independent insurance broker (not tied to a single carrier) can give you an objective view of your options.

- Revisit as life changes — Got married? Had a child? Changed jobs? Your coverage needs evolve. What made sense at closing may need an update two years later.

A Note From Simmi

When I work with buyers on the Eastside — whether they're first-time homeowners or experienced move-up buyers — my job doesn't end at closing. I genuinely care about what comes next for the families I work with, and that means encouraging conversations that go beyond square footage and offer terms.

Buying a home here is a milestone. Protecting it is a responsibility. And understanding both is part of what it means to be a truly informed homeowner in one of the most dynamic real estate markets in the country.

Share this post with anyone you know who's recently bought — or is thinking about buying — in Sammamish, Kirkland, Bellevue, Redmond, or Issaquah. This is the kind of information that should come standard with every set of keys.

Have questions about buying, selling, or navigating homeownership on the Eastside of Seattle? Simmi has guided 300+ homeowners through every stage of the process — and she's always happy to point you in the right direction. 📧 simmi@simmirealestate.com | 📞 425-324-6466

For informational purposes only. Please consult a licensed financial advisor or insurance professional for advice specific to your situation.

Our Other Blogs:

Your Complete Buyer & Seller Guide - Read More

You May Have $600K–$750K in Equity — Here's What to Do With It - Read More

8 Signs a Home Has Been Neglected - Read More

|

or another way